GRIMSBY, Ontario, June 11, 2025 (GLOBE NEWSWIRE) — Andrew Peller Limited (TSX: ADW.A / ADW.B) (“APL” or the “Company”) announced today results for the three and 12 months ended March 31, 2025. All amounts are expressed in Canadian dollars unless otherwise stated.

(MENAFN– ACCESSWIRE) NEW YORK CITY, NY / ACCESS Newswire / June 11, 2025 / New to The Street, one of the nation’s longest-running business television platforms, proudly announces a new multi-part media series spotlighting Lahontan Gold Corp. (TSX-V:LG)(OTCQB:LGCXF) and its Founder, President, and CEO Kimberly Ann Arntson . The new campaign begins filming Thursday, June 12th from the iconic New York Stock Exchange (NYSE) and will feature national television broadcasts, earned media placements, custom-produced commercials , and expansive social media distribution across all major platforms.

The announcement marks a renewed and expanded collaboration between Lahontan Gold and New to The Street, building on prior successful media appearances. As part of this enhanced engagement, the series will integrate New to The Street’s NewsOutTM video press release platform, increasing the company’s visibility to institutional investors, retail audiences, and global media outlets.

The new series will air as sponsored programming on Fox Business Network and Bloomberg Television , and will be distributed to New to The Street’s rapidly growing base of over 2.5 million YouTube subscribers . In addition, select segments will be amplified through outdoor placements across Times Square , Wall Street , and midtown Manhattan , as well as through targeted media placements with ABC, NBC, CBS, and FOX local affiliates.

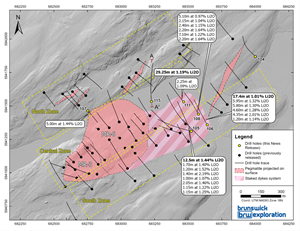

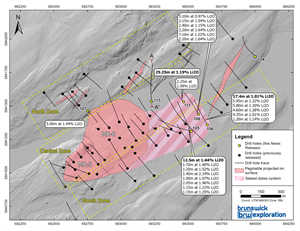

The content will feature in-depth interviews with Kimberly Ann Arntson, highlighting Lahontan’s exploration strategy in Nevada’s prolific Walker Lane District, ongoing drilling results, and the company’s plans for growth and shareholder value creation.

Broadcast air dates and digital release schedules will be announced in the coming days.

About Lahontan Gold Corp. Lahontan Gold Corp. is a Canadian exploration company focused on the development of high-grade gold and silver assets in Nevada. The company’s flagship Santa Fe Project lies within the highly prospective Walker Lane District, a region renowned for its rich mining history and ongoing gold discoveries. Led by CEO Kimberly Ann Arntson, Lahontan is rapidly advancing its exploration efforts to unlock shareholder value through responsible and aggressive project development.

Website:

About New to The Street New to The Street is a nationally recognized media platform that produces and distributes in-depth interviews and features on innovative public and private companies. Now in its 16th year, the show airs weekly as sponsored programming on Bloomberg Television , Fox Business Network , and digital outlets. With over 2.5 million YouTube subscribers , iconic Times Square billboard presence, and media partnerships across major networks, New to The Street is the go-to outlet for executive storytelling and financial news. The platform also manages NewsOutTM , a leading video press release syndication service that combines visual content with guaranteed media reach.

For media inquiries or interview opportunities: Monica Brennan PR Director, New to The Street

One of the world’s biggest consultancy firms has agreed a £281 million acquisition of Ricardo, delivering a windfall for an activist shareholder that had been seeking to oust the company’s chairman.

WSP Global has struck a surprise 430p per share cash deal for Ricardo, a smaller London-listed engineering consultancy that traces its roots back to making engines for British First World War tanks.

WSP, which is valued at C$35 billion (£19 billion) on the Toronto stock exchange, said the offer was a 28 per cent premium to Ricardo’s share price on Tuesday and a 69 per cent premium to its average price over the past three months.

The deal has been recommended by Ricardo’s board and has the backing of its biggest shareholders, making a takeover likely.

Shares in Ricardo closed up 93p, or 27.8 per cent, at 428p on Wednesday evening.

Advertisement

Science Group, a fellow London-listed science and technology consultancy, which has quickly built a stake of more than 20 per cent in Ricardo since February and launched a campaign to remove Mark Clare, Ricardo’s chairman, has agreed to sell most of its shares to WSP at the offer price.

Mark Clare had earlier accused Science Group of opportunism

Science Group has also agreed to adjourn a shareholder meeting next week on the future of Clare, 67, the former boss of Barratt Developments, the housebuilder, who is also chairman of Grainger, the FTSE 250 property company, and a senior independent director of Wickes, the retailer.

WSP employs about 72,600 people in more than 50 countries, providing engineering and strategic advisory services to clients across the transportation, infrastructure, environment, building, energy, water and mining and metals sectors.

It has expanded through about 180 acquisitions and was acquired by Genivar, a Canadian rival, in 2012 to gain a foothold in the UK market, before adopting its name.

WSP said Ricardo would bolster its capabilities in rail and transportation and environmental and energy where there was “limited overlap” between the two advisory businesses. It said it would also deliver cost savings and revenue enhancements.

Advertisement

WSP said Ricardo had “niche areas of high value expertise”, including policy, strategy and economics and would also particularly strengthen WSP’s presence in the UK, Australia and the Netherlands.

The deal could lead to the disposal of Ricardo’s automotive and industrial business, and WSP said it would “work with Ricardo’s management team to complete their strategic review of these business units”.

WSP has received irrevocable undertakings to vote in favour of the deal from Ricardo shareholders Gresham House Asset Management, Aberforth Partners and Royal London Asset Management speaking for almost 45 per cent of the stock.

Schroders, which owns about 3 per cent of Ricardo, has also backed the deal. Andy Brough, the veteran fund manager at Schroders, came out in support of attempts by Science Group to oust Clare last week.

Recommending the acquisition to Ricardo shareholders, Clare said that “while good progress has been made, there are further steps required to complete the transformation which bring some execution risks against the background of short-term market challenges and the uncertain geopolitical and macroeconomic backdrop”.

Advertisement

He added: “Against this background, WSP has made a compelling offer which represents a highly attractive premium to recent average trading levels and provides certain value in cash today for Ricardo shareholders. Importantly, the Ricardo directors believe that the acquisition will provide enhanced career opportunities for Ricardo’s employees within the WSP Group as well as access for our clients to a broader service offering.”

The deal is set to bring to an end a public dispute between Ricardo and Science Group. The latter had attacked the alleged poor performance, ineffective governance and destruction of shareholder value at Ricardo. That had prompted Ricardo to accuse Science Group of opportunism, aggressive tactics and attempting to take control “without paying a takeover premium”.

Science Group said it expected to receive about £53.5 million from its stake, generating a pre-tax net return of about 70 per cent. It said the offer price was a 102 per cent premium to Ricardo’s share price before Science Group began its stake building and campaign.

It said its board, led by Martyn Ratcliffe, Science Group’s executive chairman, intended to use the funds for “future strategic investments and corporate opportunities”.

Analysts at Canaccord Genuity, Science Group’s adviser, said the cash should provide a “sizeable war chest with further M&A”.

A group of Reitmans Ltd. shareholders have released their second letter in two months urging the apparel retailer to address its stagnating value, saying they want to replace two board directors and end the company’s dual-class share structure.

The open letter published Wednesday is from Donville Kent Asset Management Inc., Parma Investments Ltd. and an unnamed private investor. They collectively own more than 5.5 million class A shares in Reitmans and another 1.1 million common shares in the company.

In the letter, they reiterated their claim from a May 13 letter that Reitmans has demonstrated “consistently poor decision making” and ignored their requests to explore how the company could unlock more value for shareholders.

A Reitmans clothing store is seen, Tuesday May 19, 2020 in Montreal. THE CANADIAN PRESS/Ryan Remiorz

As of May 12, the company’s market capitalization was $105 million — lower than its net cash holdings of $158 million, and well below its net worth on paper of $280 million, the concerned shareholders say. This means the business was valued at less than the cash it held.

To boost the way the market perceives the retailer, the shareholders want the company to drop its dual-class share structure and move from the TSX Venture Exchange, “a junior market typically suited for emerging companies,” to the main Toronto Stock Exchange.

In response to the May letter, Reitmans said it has been in communication with Donville Kent and Parma for many quarters and “regularly evaluates options to optimize shareholder returns.”

But the shareholders maintain boosting the company’s value has fallen by the wayside because of executive chairman Stephen Reitman and his alleged “complete dominance overboard members.”

Reitman is the grandson of the company’s founders, Herman and Sarah Reitman. His family owns, on an aggregate basis, the equivalent of 21.67 per cent of the company’s shares, including a majority of the voting common shares.

Stephen Reitman has worked at the retailer for about 50 years and is well into his seventies.

He held the CEO job when the almost 100-year-old business filed for creditor protection in May 2020, citing the COVID-19 pandemic as one of the reasons for its recent woes.

The Montreal-based company rebounded after a restructuring but in order to survive it had to close 160 stores, cut 1,400 employees and dump its Addition Elle and Thyme Maternity brands. Its RW & Co. and Penningtons banners remain.

The shareholders behind the Wednesday letter argue it’s now time for the company to collapse its dual-class share structure and graduate to the Toronto Stock Exchange.

They say a TSX listing would elevate Reitmans’ profile among investors, including large institutions, result in a more accurate valuation of shares and provide it with more room to grow.

They also want a board shake up and say they are intending to vote against the reappointment of Bruce Guerriero and Daniel Rabinowicz “due to independence issues and a clear misalignment with the interests of all shareholders.”

Instead, they’d like to see Jesse Gamble, senior vice-president at Donville Kent Asset Management, and Deborah Honig, president at Adelaide Capital, join the board as independent directors.

In response, Reitmans says its ownership structure has been in place for many years and independent board members have long provided deep expertise to the business.

“We would like to stress in the strongest possible terms our confidence in the performance and objectivity of each of our independent directors and that any allegations that have recently been made impugning the independence of certain of our independent directors are false and wholly without merit,” the company said in a statement.

“There should be no doubt whatsoever as to this fact, and (we) categorically reject any assertion to the contrary.”

Since their first open letter was sent on May 13, the concerned shareholders say they have racked up support from organizations and people holding nearly 41 per cent of the shares not held by the Reitman family.

This report by The Canadian Press was first published June 11, 2025.

(MENAFN– Newsfile Corp)

Toronto, Ontario–(Newsfile Corp. – June 11, 2025) – NexMetals Mining Corp. (TSXV: NEXM) (OTC Pink: PRMLF) (” NEXM ” or the ” Company “) is pleased to announce that pursuant to its news release dated June 9, 2025, the Company’s common shares will commence trading at the market open today on the TSX Venture Exchange under the new symbol ” NEXM “.

NEXM Engages OGIB Corporate Bulletin

The Company has entered into a services agreement with OGIB Corporate Bulletin (” OGIB “) to provide strategic digital marketing services to the Company including content development and distribution, as well as campaign reporting and optimization, for a term of up to nine months. The Company has agreed to pay OGIB a total cost of CAN $40,000 in advance for these services which will be paid out of the Company’s working capital.

OGIB is wholly-owned by Keith Schaefer and is based out of Victoria, British Columbia. Both Mr. Schaefer and OGIB are arms length to the Company and, to the Company’s knowledge, hold no interest, directly or indirectly, in the securities of the Company or any right or present intention to acquire such an interest. The appointment of OGIB is subject to approval by the TSX Venture Exchange.

About NexMetals Mining Corp.

NexMetals Mining Corp. is a mineral exploration and development company that is focused on the redevelopment of the previously producing copper, nickel and cobalt resources mines owned by the Company in the Republic of Botswana.

NexMetals is committed to governance through transparent accountability and open communication within our team and our stakeholders. NexMetals’ team brings extensive experience across the full spectrum of mine discovery and development. Collectively, the team has contributed to dozens of projects, including work on the Company’s Selebi and Selkirk mines. Senior team members each have on average, more than 20 years of experience spanning geology, engineering, operations, and project development.

For further information about NexMetals Mining Corp., please contact:

Morgan Lekstrom CEO and Director …

Jaclyn Ruptash V.P., Communications and Investor Relations …

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release. No stock exchange, securities commission or other regulatory authority has approved or disapproved the information contained herein.

Follow Us X: LinkedIn: Facebook:

To view the source version of this press release, please visit

WINNIPEG, Manitoba, June 10, 2025 (GLOBE NEWSWIRE) — (TSX: NWC): The North West Company Inc. (the “Company” or “North West”) today reported its unaudited financial results for the first quarter ended April 30, 2025. It also announced that the Board of Directors has declared a quarterly dividend of $0.40 to shareholders of record on June 27, 2025, to be paid on July 15, 2025.

“Our strong first quarter performance reflects the continued momentum across our business,” said Dan McConnell, President & CEO. “Same-store sales growth and improved execution focused on meeting customer needs drove increased earnings and built on the solid foundation we established in the first quarter of last year. We’re especially encouraged by the progress we’ve made in improving on-shelf availability and refining our merchandise assortment. While it’s still early, we’re confident that our focus on operational excellence through the Next 100 initiative is the right strategy — one that will deliver meaningful value to both our customers and our shareholders. Finally, I want to acknowledge the communities affected by the wildfires in northern Canada. Our thoughts are with those impacted, and we extend our heartfelt thanks to the firefighters, community leaders, and everyone working tirelessly to protect residents and ensure their safety.”