This move is anticipated to generate enhanced cash flow and provide significant cash generation to fund DPM’s growth and capital returns programme. Credit: MacroEcon/Shutterstock.

Dundee Precious Metals (DPM) has agreed to acquire all issued shares of Adriatic Metals in a transaction valued at approximately $1.3bn (C$1.77bn).

The transaction is expected to enhance DPM’s production capacity and extend its mineral reserve life through the 100% acquisition of the Vareš silver-lead-zinc-gold mine in Bosnia and Herzegovina.

Shareholders of Adriatic Metals will receive 0.1590 of a DPM common share and 93 pence in cash for each Adriatic share under the acquisition.

The transaction implies a value of £2.68 ($3.62) per Adriatic share and A$5.56 ($3.62) per CHESS Depository Interest, based on the exchange rates as of 11 June 2025.

The scheme of arrangement under the UK Companies Act 2006 will see DPM shareholders owning approximately 75% and former Adriatic Shareholders around 25% of the enlarged issued share capital post-transaction.

This strategic move is anticipated to generate enhanced cash flow and provide significant cash generation to fund DPM’s growth and capital returns programme.

Dundee Precious Metals president and CEO David Rae said: “Adding Adriatic’s Vareš operation to our strong asset portfolio creates a premier mining business with a peer-leading growth profile, high-quality development and exploration pipeline and a robust platform to deliver above-average returns.

“Vareš is a logical fit with our portfolio, as it significantly increases DPM’s mine life while adding near-term production growth, a highly prospective land package and cash flow diversification. We are well-positioned to leverage our expertise in underground mining, our regional presence, successful track record of building and ramping up new mines, as well as our strong financial position to further optimise the operation and realise Vareš’ full value potential, based on our analysis.”

Vareš is an underground mine with an offsite processing facility located near Sarajevo and has been ramping up production since its first concentrate production in 2024.

The operation, with a 15-year initial operating life and a 4,400-hectare land package, is expected to bolster DPM’s production to as much as 425,000 gold equivalent ounces by 2027.

The independent technical report by SRK Consulting (UK), effective as of 1 April 2025, confirms Vareš’s potential with an all-in sustaining cost of $893/oz of gold equivalent.

Adriatic Metals managing director and CEO Laura Tyler said: “Vareš remains firmly on track to become a low-cost precious metal producer, underpinned by a long mine life, a high-grade deposit and strong exploration potential.

“What makes Vareš so exciting is that it is at the beginning of its journey, with significant growth potential ahead. This transaction brings together complementary strengths to create a dynamic and diversified mining company with meaningful scale. We see clear synergies between the asset portfolios of DPM and Adriatic, supported by DPM’s strong financial capacity and proven operational expertise.”

The completion of the acquisition is subject to several conditions including approvals from Adriatic Shareholders, the court, the Toronto Stock Exchange and the Bosnian Competition Council.

The transaction is expected to become effective no later than 31 December 2025.

In September last year, DPM sold its Tsumeb smelter in Namibia to a subsidiary of China’s Sinomine Resource Group for $20m.

Sign up for our daily news round-up!

Give your business an edge with our leading industry insights.

Mining Technology Excellence Awards – Have you nominated?

Nominations are now open for the prestigious Mining Technology Excellence Awards – one of the industry’s most recognised programmes celebrating innovation, leadership, and impact. This is your chance to showcase your achievements, highlight industry advancements, and gain global recognition. Don’t miss the opportunity to be honoured among the best – submit your nomination today!

The report outlines measurable progress in emissions management, resource efficiency, employee engagement, and community impact across its global operations, reinforcing HPS’s commitment to sustainability and responsible growth.

GUELPH, ON (June 12, 2025) — Hammond Power Solutions (HPS), a leader in dry-type transformers and power quality solutions, has released its 2024 Environmental, Social, and Governance (ESG) Report. The report outlines measurable progress in emissions management, resource efficiency, employee engagement, and community impact across its global operations, reinforcing HPS’s commitment to sustainability and responsible growth.

“Our updated Vision and Mission are deeply aligned with our ESG priorities, simplifying electrification, shaping sustainable power solutions, and partnering with our customers and suppliers to drive meaningful environmental impact. Our 2024 ESG Report reflects the progress we are making to support a more resilient, inclusive, and low-carbon future,” said Adrian Thomas, CEO of Hammond Power Solutions

In 2024, HPS expanded operations with new and upgraded facilities, yet limited Scope 1 and 2 emissions growth by only 10 percent, meeting its internal target. The company also improved global carbon intensity by 3 percent.

Energy efficient upgrades and operational improvements led to emissions reductions at key sites including Guelph, Baraboo, Walkerton, and Aberfoyle. Notably, a redesigned shipping skid project at the Monterrey, Mexico plant saved 42 tons of wood, equivalent to 240 pine trees.

HPS’s commitment extends beyond the environment. Employees contributed nearly 3,000 volunteer hours in 2024, while corporate giving topped $322,000 CAD. The company earned Great Place to Work certification in Canada, the U.S., and India, and continues to strengthen diversity, equity, and inclusion initiatives globally.

The full 2024 ESG Report is available here detailing HPS’s ongoing efforts to build a sustainable future through innovation and responsibility.

ABOUT HAMMOND POWER SOLUTIONS INC.

Hammond Power Solutions Inc. (“HPS” or the “Company”) enables electrification through its broad range of dry-type transformers, power quality products and related magnetics. HPS’ standard and custom-designed products are essential and ubiquitous in electrical distribution networks through an extensive range of end-user applications. The Company has manufacturing plants in Canada, the United States (U.S.), Mexico and India and sells its products around the globe. HPS shares are listed on the Toronto Stock Exchange and trade under the symbol HPS.A.

Canada’s main stock index declined on Friday, dragged down by losses in technology shares, as Israel’s widescale strikes on Iran dampened global risk appetite.

The S&P/TSX composite index was down 0.5% at 26,490.64 points.

Israel has warned that the strikes were the start of a prolonged operation to prevent Tehran from building an atomic weapon. Iran has promised a harsh response.

However, U.S. President Donald Trump urged Iran to make a deal over its nuclear programme, saying there was still time for the country to prevent further conflict with Israel.

The downturn in the TSX was limited as investors shifted to safe-haven assets, boosting metal mining shares. The materials sector gained 0.6%

The energy sector rose 1.7% to be the top gainer as the tensions in the Middle East sparked worries about supply disruptions, boosting crude prices.

“I don’t think it’s any surprise that Toronto Stock Exchange is going to hold up greater than New York, which is more based on technology or multinational corporations,” said Allan Small, senior investment advisor at Allan Small Financial Group with iA Private Wealth.

“Gold and oil make up a big chunk of our market and anything commodities-based is relatively going to do well”.

The technology sector fell 1.5%, while the heavyweight financial stocks were down nearly 1%.

The benchmark index achieved a second consecutive record high on Thursday and appears poised to secure its third straight weekly gain, provided losses remain contained.

Altus Group employees ring the bell to open the Toronto Stock Exchange in celebration of the firm’s 20th year as a publicly traded company. (Courtesy Altus Group)

Altus Group (AIF-T) marked two decades of constant growth, adaptation and technological advancements within its business when it recently celebrated 20 years as a publicly traded company.

Members of Altus Group’s executive team rang the opening bell on the Toronto Stock Exchange on May 6 to mark the date of its 20th anniversary on the exchange.

Jorge Blanco, the commercial real estate service and technology provider’s New Jersey-based chief strategy officer, was at the company’s Toronto headquarters recently and spoke with RENX about Altus’ past, present and future.

“If you look at the different chapters, the story — from the acquisition of the PricewaterhouseCoopers valuation compliance practice to the acquisition of ARGUS and the continued growth of what was the property tax business until we divested the company — has been preoccupied primarily with how we assist our clients improve their performance vis-a-vis their commercial real estate portfolio,” Blanco said.

“That’s been one constant.”

Acquisitions have been important

Altus has made more than 50 acquisitions since its inception, some large though the majority have been relatively small. That has helped the company enter new international markets and expand its suite of services with additional complementary capabilities.

The 2011 acquisition of ARGUS Software, Altus’ largest to that point, began the strategic pivot to serve the commercial real estate industry with technology to complement its valuation advisory services.

Other key acquisitions since then include:

RealNet in 2014, which enhanced Altus’ data and market research and bolstered its technology stack;

Finance Active in 2021, which expanded Altus’ debt software capabilities;

StratoDem Analytics and Reonomy in 2021, which added artificial intelligence and machine learning technology while expanding data capabilities to solve challenges with real-time data-driven insights and predictive analytics capabilities;

and Forbury in 2023, which introduced software with cloud-based solutions tailored for the Asia-Pacific market to help users make informed decisions on when best to refinance, refurbish, reposition or divest their assets.

Over the past four years, Altus has made significant investments in data standardization, integration and data science. This has enabled it to develop a sharper focus on leveraging its technology, analytics and expertise to elevate its global intelligence platform and assist clients with enhancing decision-making, mitigating risks and achieving higher returns.

“Altus is continuously evolving — modernizing our own capabilities, acquiring those that bolster our platform, and anticipating what’s next,” Blanco said. “We’re not just keeping pace with change, we’re helping define what’s next for commercial real estate through smarter technology, deeper data and a bold vision for what’s possible.”

Blanco left KPMG in New York City in March 2021 to join Altus as its executive vice-president and chief product officer. He was named chief strategy officer in February.

“My job is to ensure that I’m keeping the company about three or four steps ahead of the customer in what’s coming,” Blanco explained. “If I’m thinking about something that happened three days ago, I’m not doing my job. I need to be thinking three, five and 10 years out.”

Recent innovations and looking forward

Altus recently expanded its ARGUS Intelligence capabilities into benchmarking to provide access to insights to enhance acquisition, disposition and investment management strategies. It’s only available in the United States now but will soon follow into Canada.

“Analytics is a core component to that, as our clients want to do much more rapid simulation of the potential decisions that you could make,” Blanco said. “We all know these assets are not movable.

“They’re reshapable, but they’re not movable. So clients need to begin to consider all of the different factors that impact their value.”

While Altus isn’t currently contemplating taking its technology and expertise and adapting it for new industries, there are adjacent businesses related to commercial real estate where it could make future inroads.

“When you look at the full value chain, a lot of sectors that are not necessarily commercial real estate by nature — be it insurance, commercial lending, banking or debt investing — there are lots and lots of spaces that definitely are in our wheelhouse on areas that we should be supporting,” Blanco said.

“While we will remain very focused on the expertise we have around properties, assets, et cetera, there will be an expansion of these services that will become much more consumable for folks that are not necessarily directly in the commercial real estate space.”

Sale of property tax business

Altus closed the $700-million sale of its property tax business to Dallas-based Ryan on Jan. 2, accelerating its transformation into a pure-play software, data and analytics platform.

Some of the sale proceeds have been reinvested in buying its own stock because leadership is bullish on Altus’ future prospects.

“The emphasis that we’ve put on free cash flow per share, combined with the capital on the balance sheet, gives us a lot of optionality to continue to grow, experiment and innovate,” Blanco said.

Altus has a market cap of approximately $2.5 billion.

“It has continued to perform, but it could always perform better,” Blanco said. “We definitely think that there are other companies out there that get better multiples than we do.”

Blanco acknowledged parts of the commercial real estate industry have struggled over the past couple of years and that economic uncertainty is impacting monetary policy and growth.

“If you look at the fundamentals of the company, we’ve been growing top line and we’ve been growing bottom line consistently for a number of years, essentially meeting all the expectations of the market.”

Mantrac Group Renews 3-Year Partnership with Symbiant Following Successful Global GRC and Audit Software Implementation – Toronto Stock Exchange News Today – EIN Presswire

Trusted News Since 1995

A service for global professionals · Friday, June 13, 2025

· 821,951,112

Articles

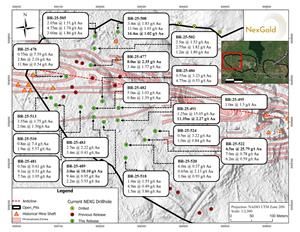

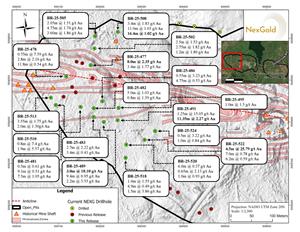

NexGold Infill Drilling Intersects 25.79 g/t Gold Over 4.5 Metres and 18.09 g/t Gold over 3.0 Metres at the Goldboro Gold Project – Toronto Stock Exchange News Today – EIN Presswire

Trusted News Since 1995

A service for global professionals · Friday, June 13, 2025

· 821,878,804

Articles