Bitfarms’ board approved a share buyback of up to 49.9 million shares.

Bitfarms (BITF) CEO Ben Gagnon believes the company’s stock is trading below its intrinsic value, as the market is overlooking the value of its Bitcoin operations.

“We believe that Bitfarms’ shares are currently undervalued because our Bitcoin business is underappreciated by the market, with little to no value being associated with our HPC potential,” said CEO Ben Gagnon.

The comment came on Tuesday, after the company’s Board of Directors approved a share repurchase initiative, authorizing a buyback of up to 49.9 million of its common shares, equivalent to roughly 10% of its public float.

Following the announcement, Bitfarms stock traded over 17% higher in Tuesday morning after the bell.

On Stocktwits, retail sentiment toward Bitfarms jumped to ‘bullish’ from ‘bearish’ territory the previous day. Message volume levels improved to ‘high’ from ‘normal’ levels in 24 hours.

BITF’s Sentiment Meter and Message Volume as of 09.15 a.m. ET on July 22, 2025 | Source: Stocktwits

Bitfarms’ message count surged 887% in the last 24 hours.

A Stocktwits user expressed optimism about the buyback plans.

The Toronto Stock Exchange (TSX) has greenlit the buyback plan, allowing the company to implement a normal course issuer bid beginning July 28, 2025, and running through July 27, 2026.

Bitfarms intends to carry out the buybacks on both the TSX and the Nasdaq, with purchases subject to several variables, including available liquidity and market conditions.

On the TSX, daily purchases will not exceed 494,918 shares, which amounts to 25% of the company’s average daily volume over the prior six-month period ending June 30, 2025.

Bitfarms stock has lost over 24% year-to-date and over 60% in the last 12 months.

For updates and corrections, email newsroom[at]stocktwits[dot]com.<

Canada’s main stock index was subdued on Tuesday, pressured by technology stocks, as investors awaited potential trade deals between the U.S. and its partners.

The Toronto Stock Exchange’s S&P/TSX composite index was down 0.03% at 27,307.73 points.

Trade negotiations appeared shaky after EU diplomats said the 27-nation bloc was considering broader counter-measures against Washington.

Prospects for an interim trade deal between India and the U.S. have also dimmed, according to Indian government sources.

Meanwhile, U.S. Treasury Secretary Scott Bessent announced plans to meet his Chinese counterpart next week, potentially discussing an extension to the August 12 deadline set for tariffs on China.

The Bank of Canada said in a survey Canadian businesses see less chance of a worst-case tariff scenario but remain cautious, while keeping hiring and investment in check.

“The TSX should do relatively well throughout this earnings period,” said Ian Chong, portfolio manager at First Avenue Investment Counsel.

He added that while there will be a tariff impact, it will be “relatively muted” since the full-blown 35% tariff on Canada has not been set yet.

On the TSX, materials stocks gained 1.1% after gold prices retreated from a five-week high.

Conversely, the information and technology subindex slipped 1.8%, tracking declines in its Wall Street peers.

In the U.S., Alphabet and Tesla will kick off the results season for the “Magnificent Seven” stocks on Wednesday.

The

cryptocurrency market has witnessed a strong momentum in July 2025, with XRP

leading the charge among major digital assets. Why is XRP going up? The answer

lies in a perfect storm of regulatory breakthroughs, institutional adoption,

and technical breakouts that have propelled XRP to almost all-time highs above

$3.60.

Moreover,

the technical analysis now suggests that XRP’s price may continue to rise,

potentially heading toward levels above $6.

XRP has

established itself as a standout performer in the cryptocurrency space,

currently trading at $3.47 with a market capitalization of $204.39 billion. The

digital asset has demonstrated exceptional resilience, gaining over 474% in the

past year and maintaining its position as the fourth-largest cryptocurrency by

market cap.

XRP

price today. Source: CoinMarketCap.com

Recent

price action tells a compelling story. XRP hit a new all-time high of $3.84 in

January 2018, but the current rally has brought it tantalizingly close to those

levels. The token has surged 21% over the past seven days, with trading volumes

reaching $9.74 billion in 24-hour periods.

Market

dynamics reveal strong institutional interest. XRP rebounded sharply from the

$3.40 support zone following initial profit-taking, with buyers stepping in

aggressively at volume levels nearly triple the daily average. This pattern

suggests conviction buying at key technical levels.

Regulatory Breakthrough:

The SEC Settlement Game-Changer

The most

significant catalyst behind XRP’s surge stems from regulatory clarity. In March

2025, Ripple Labs settled its long-standing lawsuit with the Securities and

Exchange Commission, agreeing to pay a $50 million fine. This resolution

effectively ended the legal battle that had suppressed XRP’s price for years.

The

settlement confirmed that XRP is not a security in the context of secondary

market sales. This clarification removed major regulatory uncertainty that had

previously led exchanges to delist XRP from their platforms. Following the

settlement, major U.S. exchanges resumed XRP trading with renewed confidence.

Ripple CEO

Brad Garlinghouse noted that institutions were “finally seeing Ripple with

confidence” and returning to partnerships. The regulatory green light has

unlocked institutional adoption that was previously hampered by compliance

concerns.

ETF Revolution: Wall

Street Embraces XRP

The launch

of XRP exchange-traded funds represents another pivotal development driving

price momentum. The ProShares Ultra XRP ETF received approval for listing on

the New York Stock Exchange under ticker UXRP. This marked a significant shift

in the SEC’s approach to cryptocurrency-based financial products.

Currently,

four XRP ETFs trade in U.S. markets, providing institutional and retail

investors with regulated exposure to XRP price movements. The ETF ecosystem has

experienced explosive growth, with XRP ETFs surging more than 50% in one month.

Bloomberg analysts suggest an 85% chance of spot XRP ETF approval in 2025,

which could trigger substantial additional demand.

The Purpose

XRP ETF also launched on the Toronto Stock Exchange under ticker XRPP,

expanding international access to XRP through regulated investment vehicles.

This institutional infrastructure development represents a fundamental shift in

how traditional finance views digital assets.

XRP Price Technical Analysis:

Bullish Outlook Toward $6.19 if $3.60 Resistance Breaks

According

to my recent technical analysis, the XRP price approached the $3.60 mark this

month and stalled, forming almost new historical high and establishing a key

resistance zone at this level.

However, if

we trust the Fibonacci extension levels based on the bullish trend from the

June lows to the current highs, and the subsequent correction, the medium-term

outlook suggests that XRP may continue its upward trajectory, potentially

surpassing $6.00.

Key

Fibonacci Extension Levels (from June lows to current highs):

Extension

Level

Price

Target

50%

$4.20

61.8%

$4.41

100%

$5.09

161.8%

$6.19

Given this,

my medium-term projection for XRP is around $6.19. From the current price

levels, that would represent an increase of $2.70, or approximately 80%.

What Could Invalidate This

XRP Bullish Scenario?

The first

warning signal that bulls may be losing momentum would be a drop below the

psychological support level at $3.00, which aligns with the March 2025 highs.

If this support fails, the next likely target would be:

$2.60 – where the 50-day EMA and May

2025 highs are located

$2.26

– near the 200-day EMA

A confirmed

breakdown below $3.00 would open the door for a more significant bearish

retracement.

Whether XRP

moves higher or faces a deeper correction will likely be decided at the $3.60

resistance level. A breakout above this mark, without a sharp pullback below $3.40

(January 2025 highs), would strongly increase the odds of the bullish scenario

playing out.

XRP Flag Pattern Suggests $5.25

XRP recently broke out of a

flag pattern or ascending triangle at the beginning of July.

This breakout has been followed

by strong upward momentum, confirming the bullish breakout.

Based on the measured move from

this breakout, the next target stands around $5.25, slightly above

the 100% Fibonacci extension.

XRP Price Predictions 2025

And Beyond

The

prediction landscape reveals a clear bifurcation between institutional and

retail expectations. Traditional financial institutions like Standard Chartered

cluster around $3.40-$5.50 targets, while crypto-native influencers project

$10-$26.50 ranges. This divergence reflects different risk tolerances,

analytical frameworks, and market perspectives.

Payment utility expansion: Ripple partnership

announcements could accelerate targets

XRP News FAQ

Why Is XRP Rising in

Price?

XRP’s price

surge stems from a perfect storm of regulatory clarity, institutional adoption,

and technical momentum. The $50 million SEC settlement in March 2025 removed

years of legal uncertainty, while XRP ETF approvals have opened institutional

floodgates with over $9.74 billion in daily trading volumes. Standard

Chartered’s $5.50 price target and record whale accumulation patterns

demonstrate growing institutional confidence, while Ripple‘s expanding CBDC

partnerships and cross-border payment utility provide fundamental value drivers

beyond speculative trading.

Is XRP Going to Skyrocket?

XRP’s

trajectory suggests continued strong performance rather than parabolic

“skyrocketing,” according to institutional analysis. While crypto

influencers project targets up to $26.50, veteran trader Peter Brandt’s 60%

rally prediction to $4.47 and Standard Chartered’s measured $5.50 forecast

reflect more realistic expectations. The digital asset has already gained 474%

annually, and technical indicators show healthy consolidation around $3.47

rather than unsustainable bubble dynamics that typically precede dramatic

crashes.

Can XRP Reach $5?

XRP

reaching $5 appears highly probable based on convergent institutional and

technical analysis. Multiple credible sources including Standard Chartered,

ChatGPT algorithmic models, Arthur Azizov’s regulatory analysis, and Bitget’s

exchange data all center around $5.00 targets for 2025. This represents a

conservative 44% upside from current $3.47 levels, supported by ETF momentum,

institutional buying patterns, and the resolution of regulatory headwinds that

previously capped XRP’s growth potential.

How High Can XRP

Realistically Go?

XRP’s

realistic upside ranges from $5.50 to $10 depending on market conditions and

adoption speed. Conservative institutional forecasts cluster around Standard

Chartered’s $5.50 target, while technical analysis supports Jake Gagain’s $7.50

new all-time high prediction. Zubic’s conditional $10 target tied to Bitcoin

reaching $250K represents the upper realistic bound, as it assumes broader

crypto market momentum. Predictions beyond $15 enter speculative territory

requiring parabolic adoption curves that rarely materialize in traditional

financial markets, even within the crypto space.

The

cryptocurrency market has witnessed a strong momentum in July 2025, with XRP

leading the charge among major digital assets. Why is XRP going up? The answer

lies in a perfect storm of regulatory breakthroughs, institutional adoption,

and technical breakouts that have propelled XRP to almost all-time highs above

$3.60.

Moreover,

the technical analysis now suggests that XRP’s price may continue to rise,

potentially heading toward levels above $6.

XRP has

established itself as a standout performer in the cryptocurrency space,

currently trading at $3.47 with a market capitalization of $204.39 billion. The

digital asset has demonstrated exceptional resilience, gaining over 474% in the

past year and maintaining its position as the fourth-largest cryptocurrency by

market cap.

XRP

price today. Source: CoinMarketCap.com

Recent

price action tells a compelling story. XRP hit a new all-time high of $3.84 in

January 2018, but the current rally has brought it tantalizingly close to those

levels. The token has surged 21% over the past seven days, with trading volumes

reaching $9.74 billion in 24-hour periods.

Market

dynamics reveal strong institutional interest. XRP rebounded sharply from the

$3.40 support zone following initial profit-taking, with buyers stepping in

aggressively at volume levels nearly triple the daily average. This pattern

suggests conviction buying at key technical levels.

Regulatory Breakthrough:

The SEC Settlement Game-Changer

The most

significant catalyst behind XRP’s surge stems from regulatory clarity. In March

2025, Ripple Labs settled its long-standing lawsuit with the Securities and

Exchange Commission, agreeing to pay a $50 million fine. This resolution

effectively ended the legal battle that had suppressed XRP’s price for years.

The

settlement confirmed that XRP is not a security in the context of secondary

market sales. This clarification removed major regulatory uncertainty that had

previously led exchanges to delist XRP from their platforms. Following the

settlement, major U.S. exchanges resumed XRP trading with renewed confidence.

Ripple CEO

Brad Garlinghouse noted that institutions were “finally seeing Ripple with

confidence” and returning to partnerships. The regulatory green light has

unlocked institutional adoption that was previously hampered by compliance

concerns.

ETF Revolution: Wall

Street Embraces XRP

The launch

of XRP exchange-traded funds represents another pivotal development driving

price momentum. The ProShares Ultra XRP ETF received approval for listing on

the New York Stock Exchange under ticker UXRP. This marked a significant shift

in the SEC’s approach to cryptocurrency-based financial products.

Currently,

four XRP ETFs trade in U.S. markets, providing institutional and retail

investors with regulated exposure to XRP price movements. The ETF ecosystem has

experienced explosive growth, with XRP ETFs surging more than 50% in one month.

Bloomberg analysts suggest an 85% chance of spot XRP ETF approval in 2025,

which could trigger substantial additional demand.

The Purpose

XRP ETF also launched on the Toronto Stock Exchange under ticker XRPP,

expanding international access to XRP through regulated investment vehicles.

This institutional infrastructure development represents a fundamental shift in

how traditional finance views digital assets.

XRP Price Technical Analysis:

Bullish Outlook Toward $6.19 if $3.60 Resistance Breaks

According

to my recent technical analysis, the XRP price approached the $3.60 mark this

month and stalled, forming almost new historical high and establishing a key

resistance zone at this level.

However, if

we trust the Fibonacci extension levels based on the bullish trend from the

June lows to the current highs, and the subsequent correction, the medium-term

outlook suggests that XRP may continue its upward trajectory, potentially

surpassing $6.00.

Key

Fibonacci Extension Levels (from June lows to current highs):

Extension

Level

Price

Target

50%

$4.20

61.8%

$4.41

100%

$5.09

161.8%

$6.19

Given this,

my medium-term projection for XRP is around $6.19. From the current price

levels, that would represent an increase of $2.70, or approximately 80%.

What Could Invalidate This

XRP Bullish Scenario?

The first

warning signal that bulls may be losing momentum would be a drop below the

psychological support level at $3.00, which aligns with the March 2025 highs.

If this support fails, the next likely target would be:

$2.60 – where the 50-day EMA and May

2025 highs are located

$2.26

– near the 200-day EMA

A confirmed

breakdown below $3.00 would open the door for a more significant bearish

retracement.

Whether XRP

moves higher or faces a deeper correction will likely be decided at the $3.60

resistance level. A breakout above this mark, without a sharp pullback below $3.40

(January 2025 highs), would strongly increase the odds of the bullish scenario

playing out.

XRP Flag Pattern Suggests $5.25

XRP recently broke out of a

flag pattern or ascending triangle at the beginning of July.

This breakout has been followed

by strong upward momentum, confirming the bullish breakout.

Based on the measured move from

this breakout, the next target stands around $5.25, slightly above

the 100% Fibonacci extension.

XRP Price Predictions 2025

And Beyond

The

prediction landscape reveals a clear bifurcation between institutional and

retail expectations. Traditional financial institutions like Standard Chartered

cluster around $3.40-$5.50 targets, while crypto-native influencers project

$10-$26.50 ranges. This divergence reflects different risk tolerances,

analytical frameworks, and market perspectives.

Payment utility expansion: Ripple partnership

announcements could accelerate targets

XRP News FAQ

Why Is XRP Rising in

Price?

XRP’s price

surge stems from a perfect storm of regulatory clarity, institutional adoption,

and technical momentum. The $50 million SEC settlement in March 2025 removed

years of legal uncertainty, while XRP ETF approvals have opened institutional

floodgates with over $9.74 billion in daily trading volumes. Standard

Chartered’s $5.50 price target and record whale accumulation patterns

demonstrate growing institutional confidence, while Ripple‘s expanding CBDC

partnerships and cross-border payment utility provide fundamental value drivers

beyond speculative trading.

Is XRP Going to Skyrocket?

XRP’s

trajectory suggests continued strong performance rather than parabolic

“skyrocketing,” according to institutional analysis. While crypto

influencers project targets up to $26.50, veteran trader Peter Brandt’s 60%

rally prediction to $4.47 and Standard Chartered’s measured $5.50 forecast

reflect more realistic expectations. The digital asset has already gained 474%

annually, and technical indicators show healthy consolidation around $3.47

rather than unsustainable bubble dynamics that typically precede dramatic

crashes.

Can XRP Reach $5?

XRP

reaching $5 appears highly probable based on convergent institutional and

technical analysis. Multiple credible sources including Standard Chartered,

ChatGPT algorithmic models, Arthur Azizov’s regulatory analysis, and Bitget’s

exchange data all center around $5.00 targets for 2025. This represents a

conservative 44% upside from current $3.47 levels, supported by ETF momentum,

institutional buying patterns, and the resolution of regulatory headwinds that

previously capped XRP’s growth potential.

How High Can XRP

Realistically Go?

XRP’s

realistic upside ranges from $5.50 to $10 depending on market conditions and

adoption speed. Conservative institutional forecasts cluster around Standard

Chartered’s $5.50 target, while technical analysis supports Jake Gagain’s $7.50

new all-time high prediction. Zubic’s conditional $10 target tied to Bitcoin

reaching $250K represents the upper realistic bound, as it assumes broader

crypto market momentum. Predictions beyond $15 enter speculative territory

requiring parabolic adoption curves that rarely materialize in traditional

financial markets, even within the crypto space.

MONTREAL, July 22, 2025 (GLOBE NEWSWIRE) — Osisko Metals Incorporated (the “Company” or “Osisko Metals”) (TSX-V: OM; OTCQX: OMZNF; FRANKFURT: 0B51) is pleased to announce new drill results from the Gaspé Copper Project, located in the Gaspé Peninsula of Eastern Québec.

Osisko Metals Chief Executive Officer Robert Wares commented: “These new results underscore the overall large-scale potential of mineralization at Gaspé Copper, with drill hole 1082 cutting 853 metres of continuous mineralization, including the bottom 424 metres being located immediately below and outside the 2024 MRE model. Furthermore, drill hole 1088 intersected new mineralization 80 metres southwest of the 2024 MRE model, emphasizing the excellent potential for increasing the size of the known deposit at depth and to the south.”

The content in this section is supplied by Newsfile for the purposes of distributing press releases on behalf of its clients. Postmedia has not reviewed the content.

Calgary, Alberta–(Newsfile Corp. – July 21, 2025) – 1317234 B.C. Ltd. (the “Company“) is pleased to announce that it has entered into a non-binding letter of intent (the “LOI“) with Marviken Ontario Inc. (“Marviken“) which outlines the terms and conditions of a proposed business combination of Marviken and the Company by way of a three-cornered amalgamation, which will result in a reverse take-over of the Company by the shareholders of Marviken (the “ProposedTransaction“) pursuant to the policies of the TSX Venture Exchange (the “Exchange” or the “TSXV“). In connection with the Proposed Transaction, the Company will apply to list its common shares on the TSXV by way of a direct listing.

Advertisement 2

Story continues below

This advertisement has not loaded yet, but your article continues below.

THIS CONTENT IS RESERVED FOR SUBSCRIBERS

Subscribe now to read the latest news in your community.

Unlimited online access to all articles on thewhig.com.

Access to subscriber-only content, including History: As We Saw It, a weekly newsletter that rips history from our archives, which span almost 190 years.

Enjoy insights and behind-the-scenes analysis from our award-winning journalists.

Support local journalism and the next generation of journalists.

SUBSCRIBE TO UNLOCK MORE ARTICLES

Subscribe now to read the latest news in your community.

Unlimited online access to all articles on thewhig.com.

Access to subscriber-only content, including History: As We Saw It, a weekly newsletter that rips history from our archives, which span almost 190 years.

Enjoy insights and behind-the-scenes analysis from our award-winning journalists.

Support local journalism and the next generation of journalists.

REGISTER / SIGN IN TO UNLOCK MORE ARTICLES

Create an account or sign in to keep reading.

Access more articles from thewhig.com.

Share your thoughts and join the conversation in the comments.

Get email updates from your favourite journalists.

THIS ARTICLE IS FREE TO READ REGISTER TO UNLOCK.

Create an account or sign in to continue with your reading experience.

Access articles from across Canada with one account

Share your thoughts and join the conversation in the comments

Enjoy additional articles per month

Get email updates from your favourite authors

Sign In or Create an Account

or

Article content

Marviken owns 100% of the issued and outstanding shares of Marviken One AB (“Marviken SE“), a company incorporated under the laws of Sweden, that is the owner of a fourteen (14) acre site (the “Marviken SmartEnergy Cluster“) strategically located south of Stockholm, Sweden. The Marviken Smart Energy Cluster benefits from a long history of power production, existing operational battery facilities, and plans for significant expansion, including a data center and a 70 MW / 70 MWh battery energy storage system connecting via an on-site substation. Marviken is aiming to build services in the transformation of the Swedish energy landscape, driven by a significant need to address grid reliability.

The Proposed Transaction

The Kingston Whig-Standard’s Noon News Roundup

Your weekday lunchtime roundup of curated links, news highlights, analysis and features.

By signing up you consent to receive the above newsletter from Postmedia Network Inc.

Thanks for signing up!

A welcome email is on its way. If you don’t see it, please check your junk folder.

The next issue of The Kingston Whig-Standard’s Noon News Roundup will soon be in your inbox.

We encountered an issue signing you up. Please try again

Article content

Advertisement 3

Story continues below

This advertisement has not loaded yet, but your article continues below.

Article content

Under the terms of the LOI, it is anticipated that (i) prior to the consummation of the Proposed Transaction, the Company will implement a consolidation (the “Consolidation“) of all of the issued and outstanding shares of the Company (each a “Company Share“) based on a ratio to be determined immediately prior to the closing of the Proposed Transaction (the “Consolidation Ratio“), such that the existing holders of Company Shares (“Company Shareholders“) shall hold, in the aggregate, such number of common shares of the Resulting Issuer (the “Resulting Issuer Shares“) that when multiplied by the offering price of the Concurrent Financing (as defined herein) equals $750,000; and (ii) each outstanding security of Marviken shall be exchanged on a one for one basis (the “Exchange Ratio“) for an equivalent security of the Resulting Issuer.

Advertisement 4

Story continues below

This advertisement has not loaded yet, but your article continues below.

Article content

Upon completion of the Proposed Transaction, it is expected that: (i) Marviken will become a wholly-owned subsidiary of the Company or otherwise combining its corporate existence with that of the Company to form the resulting issuer (the “Resulting Issuer“); (ii) that the Resulting Issuer Shares will be listed as a Tier 1 industrial issuer on the TSXV; and (iii) the Company will carry on the business of Marviken under the name “Marviken Energy Inc” or such other name as determined by the board of directors of Marviken and as approved by the Exchange. The Proposed Transaction is subject to the parties successfully entering into a definitive agreement in respect of the Proposed Transaction on or before September 15, 2025.

Advertisement 5

Story continues below

This advertisement has not loaded yet, but your article continues below.

Article content

Completion of the Proposed Transaction will be subject to a number of conditions, including obtaining all necessary board, shareholder and regulatory approvals, including Exchange approval, as well as the completion of the Concurrent Financing.

Concurrent Financing

Marviken will endeavor to complete a private placement offering of subscription receipts for minimum gross proceeds of $20,000,000 (or such other amount as is necessary to satisfy TSXV listing requirements) (the “Concurrent Financing“). It is anticipated that net proceeds from the Concurrent Financing will be used to fund the business of Marviken.

Board of Directors

Upon the consummation of the Proposed Transaction, the board of directors of the Resulting Issuer shall consist of five directors, all of whom will be nominated by Marviken.

Advertisement 6

Story continues below

This advertisement has not loaded yet, but your article continues below.

Article content

About 1317234 B.C. Ltd.

The Company was incorporated in the province of British Columbia on July 27, 2021. The Company is a reporting issuer but does not trade on a stock exchange. The principal business of the Company is to identify and evaluate assets or businesses with a view to potentially acquire them or an interest therein by completing a purchase transaction, by exercising of an option or by any concomitant transaction.

For further information:

Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the Exchange) accepts responsibility for the adequacy or accuracy of this news release.

Advertisement 7

Story continues below

This advertisement has not loaded yet, but your article continues below.

This news release includes certain statements that may be deemed “forward-looking statements”. All statements in this new release, other than statements of historical facts, that address events or developments that the Company expects to occur, are forward-looking statements. Forward-looking statements are statements that are not historical facts and are generally, but not always, identified by the words “expects”, “plans”, “anticipates”, “believes”, “intends”, “estimates”, “projects”, “potential” and similar expressions, or that events or conditions “will”, “would”, “may”, “could” or “should” occur and specifically include statements regarding the Proposed Transaction and the related transactions described herein, satisfaction of the conditions precedent to closing of the Proposed Transaction; the completion of the Concurrent Financing and the use of proceeds therefrom; approval of regulatory bodies; the completion of the Consolidation; the parties ability to determine the appropriate Consolidation Ratio; listing of the Resulting Issuer Shares on the TSXV; and the Company’s business and strategic plans. Although the Company believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results may differ materially from those in the forward-looking statements. Investors are cautioned that any such statements are not guarantees of future performance and actual results or developments may differ materially from those projected in the forward-looking statements. Forward-looking statements are based on the beliefs, estimates and opinions of the Company’s management on the date the statements are made. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Except as required by applicable securities laws, the Company undertakes no obligation to update these forward-looking statements of beliefs, opinions, projections, or other factors, should they change, except as required by law. The statements in this news release are made as of the date of this release.

Not for distribution to U.S. Newswire Services or for dissemination in the United States. Any failure to comply with this restriction may constitute a violation of U.S. Securities laws.

Galaxy Digital IncGLXY shares are hitting new highs on Monday after the company announced a strategic partnership with K Wave MediaKWM to accelerate its BitcoinBTC/USDtreasury strategy.

What Happened: Galaxy will serve as an asset manager and strategic advisor to K Wave Media and invest in the company.

Galaxy will provide guidance on structuring and making Bitcoin purchase, risk management and long-term institutional-grade infrastructure.

The news comes after K Wave recently acquired 88 Bitcoin as part of its Bitcoin treasury strategy. The company is planning to “aggressively” scale its Bitcoin reserves. The company said it now has access to more than $1 billion in institutional capital to support its strategic plans.

“Corporate adoption of Bitcoin is evolving from theory to action, and K Wave Media is at the forefront of that shift. Their commitment to a Bitcoin-native treasury model reflects a growing movement among forward-looking public companies,” said Steve Kurz, global head of asset management at Galaxy.

Galaxy Digital shares also appear to be getting a boost on Monday after Piper Sandler analyst Patrick Moley maintained an Overweight rating and raised the price target from $34 to $36.

Trending Investment Opportunities

Advertisement

Galaxy has traded on the Toronto Stock Exchange and OTC markets since 2020. The company was uplisted to the Nasdaq in May.

Rosenblatt analyst Chris Brendler initiated coverage on Galaxy in June with a Buy rating and set a price target of $25. Canaccord Genuity maintained a Buy rating on Galaxy at the beginning of July with a price target of $33. Galaxy has a consensus target of $31.33, according to Benzinga analyst data.

LAVAL – Alimentation Couche-Tard Inc. says it’s restarting its share buyback program after it announced last week that it had ended its efforts to acquire the owner of the 7-Eleven chain.

Laval, Que.-based Couche-Tard says the Toronto Stock Exchange had approved its program to buy back up to 10 per cent of outstanding shares that, based on its current price, represents about $5.8 billion in shares.

The company says the potential repurchasing of about 77.1 million shares is an appropriate use of its cash and an efficient way to create long-term shareholder value.

Couche-Tard had been keeping funds on-hand as it tried for more than a year to land a friendly takeover of Japan-based Seven & i Holdings Co. Ltd. in a deal that could have been worth more than $60 billion.

The company said last Wednesday it had withdrawn its proposal, citing a lack of constructive engagement from Seven & i.

Seven & i said it had engaged in good-faith discussions, but had also expressed concerns about antitrust hurdles and the broad shifts in the global economy that would challenge the prospects of any deal.

This report by The Canadian Press was first published July 21, 2025.

Dan Oberste is the CEO of BSR Real Estate Investment Trust, which is headquartered in Little Rock and trades on the Toronto Stock Exchange. (Steve Lewis)

In May 2024, the CEO of a Virginia company that owns more apartments than almost anyone in the United States made a cold call to the front desk of BSR Real Estate Investment Trust, a similar business headquartered in Little Rock’s Union Station.

About a year later, that phone call led to a whopping $618 million real estate deal that moved nine high-end apartment complexes in Texas from BSR’s portfolio into the hands of AvalonBay Communities. Maybe more importantly, the deal sent some of BSR’s early investors — and those investors’ rights to block some of BSR’s moves — to AvalonBay Communities.

BSR walked away from the transaction with a hefty pile of cash — some of which has already been spent to buy up more properties in Texas — as well as the freedom to send the company in a new direction, whatever that might be.

The ingredients are in place for other investors to take an interest in BSR, a company that trades publicly in Canada and owns thousands of high-end apartments in the desirable Texas market.

But BSR CEO Dan Oberste is careful when discussing BSR’s future, saying that selling off the company’s assets or going private are possible but so are boosting the stock price and increasing distributions to shareholders.

“BSR is for sale every day,” Oberste said, noting that any amount from one share in a company to the entire enterprise of a publicly traded company can be purchased at any time.

A Little Rock native, Oberste recalls working for BSR as a kid when it was a private company and painting the office walls for $6 an hour.

Today, Oberste is the CEO with total compensation of $1.7 million last year. While Oberste holds one of seven positions on the board, he describes himself as a professional manager whose objective is to drive shareholder return.

“You see this transition from, historically, a family business that is well-known in Little Rock to an institution run by professional managers,” Oberste said, comparing himself to a bus driver rather than an owner of the bus.

Oberste and the company’s management and board own around 6%-7% of the company. That’s a small amount of the overall pie but an “astronomically high number” compared with the typical percentage, which is less than 1%, BSR CFO Thomas Cirbus said.

BSR is a real estate investment trust, a type of company that owns income-producing real estate — like residential or commercial rental units — and pays dividends to shareholders from the income on those properties. REITS, as they are known, were created by Congress in 1960 as a way to allow retail investors to invest in large-scale real estate developments that might not otherwise be within reach.

Oberste said the management team can drive shareholder return by increasing distributions, which he said have risen by about 11% since the company went public in 2018, or by improving the value of the stock.

“If someone comes along and offers management the ability to maximize the shareholder return while mitigating the risk involved with time and execution, then it’s our job to assess that and advise the board and recommend what the company should do,” he said.

Project Cowboy

Part of BSR’s value in 2025 lies in the deal with AvalonBay Communities, because it gives the company more freedom, which had been limited due to its history as a private company.

In 1956, BSR was founded as a private company known as Bailey Corp., which went on to develop Little Rock neighborhoods such as Foxcroft and St. Charles as well as the Pavilion in the Park shopping center on Cantrell Road.

In the 1990s, John Bailey took over the company, renamed Bailey Properties in 1998, and focused on multifamily apartments with complexes in Little Rock and others in surrounding states.

In 2013, Bailey Properties merged with Summit Housing Partners LLC of Montgomery, Alabama, and changed its name to BSR Trust LLC. The company’s headquarters briefly moved to Montgomery before returning to Little Rock in the Union Station train station.

About seven years ago, BSR wanted to go public, but with about 7,000 units in its portfolio, the company is small by REIT standards. By comparison, AvalonBay Communities has more than 94,000 apartments and is the third-largest owner of apartments in the country.

BSR was too small for the New York Stock Exchange, so the company opted for the Toronto Stock Exchange and went public in May 2018. Oberste, who became the CEO about four years later, said the move made sense as BSR would take the place of another REIT that left the exchange, giving Canadians an opportunity to invest in real estate in the U.S. Sunbelt.

BSR Real Estate Investment Trust owns and operates apartments, including many high-end units in the areas in and around Dallas, Houston and Austin.

One issue for BSR was that the founding members of the company held certain rights, including the right to block certain major transactions. Known as the Bailey-Hughes affiliates, those investors controlled about 40% of the company when it went public and had the right to appoint up to three board members.

The sale this year, dubbed “Project Cowboy” by BSR, occurred in two transactions. The first sale included 857 units in the Austin area for $187 million. The second included 1,844 units in the Dallas area for $431.5 million.

The transaction also gave the Bailey-Hughes affiliates, as well as other investors who had been with the company since before it went public, an option to move to AvalonBay. After the deal, the Bailey-Hughes affiliates’ portion of BSR fell from 40% to 13%, eliminating their blocking rights. Their board-appointment rights were reduced from three board members to one.

“When you’ve got one hand tied behind your back, it makes it difficult to market that stock, because a lot of stock buyers want to buy a small REIT in hopes that it will privatize,” Oberste said.

The deal, which would have ranked No. 3 on Arkansas Business’ list of the biggest deals involving Arkansas companies in 2024, has also been good for the stock price. As of mid-July, BSR’s stock price had risen about 12.5% since the deal was announced in February.

One market analyst called the deal “transformational” and others have spoken favorably of the transaction. Several analysts noted BSR trades at a “discount” compared with its net asset value, suggesting the stock is more valuable than the company’s stock price suggests.

Lone Star Living

When BSR went public, it began to focus on Texas, a plan that has proved advantageous with the surge in Texas’ population in recent years. Last year, the U.S. Census Bureau estimated that Texas gained 562,941 residents, more than any other state.

As Texas has grown, so has the desirability of BSR’s real estate, putting the company in an enviable spot, Oberste says.

“We’ve got something that a lot of people want,” he said. “And that’s brand-new suburban Class A apartments in Texas — in Dallas, Austin and Houston.”

To understand BSR’s position, it’s important to understand some geographic trends across the Arkansas border. In simplest terms, people keep moving to Texas and BSR owns thousands of high-end apartments in the state’s fastest-growing cities.

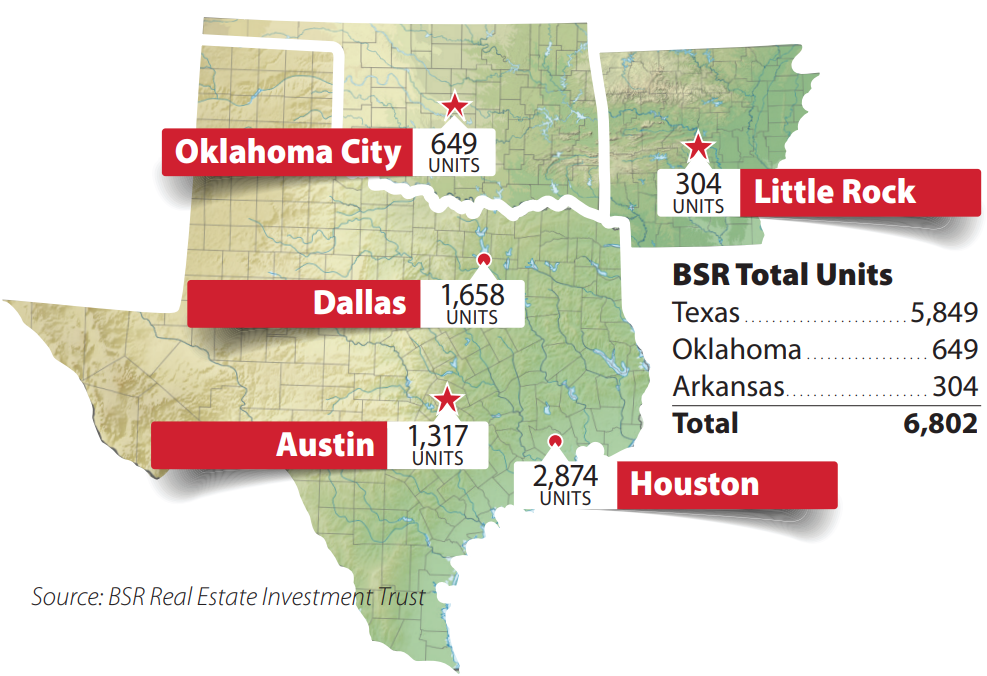

The company also owns 649 similar apartments in Oklahoma City and 304 in Little Rock, although BSR’s three Arkansas properties aren’t indicative of its fancier holdings outside the state.

According to the Texas Demographic Center, the state’s population has grown from about 29 million in 2020 to 31.6 million this year. That’s about a 9% increase in five years, according to the state agency’s most conservative estimate. The population could be as high as 36 million in 10 years and 40.6 million in 20 years, the state estimated.

But most of the growth in Texas has come in the state’s major metropolitan areas, specifically concentrated in the triangle between Dallas, Austin and Houston.

After the sale to AvalonBay, BSR bought two properties in the Houston area. The acquisitions show what type of properties BSR is interested in. Forayna Vintage Park in Houston has 350 apartment suites, and the population in a 3-mile radius has an average household income of $109,262. The company also bought Botanic Luxury, located in the Houston suburb of Spring, which has 288 apartment suites with a surrounding household income of $95,518.

The company would like to buy another property in Dallas in the next three or four months.

BSR CEO Dan Oberste said the company has more freedom with its future after the transaction with AvalonBay Communities. (Steve Lewis)

In total, BSR owns 6,802 units across 25 properties in Arkansas, Oklahoma and Texas, but the Texas units are the real prize. The company has 2,874 units in the Houston area with an average monthly rent of $1,525, 1,658 units in the Dallas area with an average rent of $1,538 and 1,317 units in the Austin area with an average rent of $1,554. In Texas, BSR had an occupancy rate of 96.1% at the end of the first quarter this year.

The rental units are more valuable in the context of the high hurdles to home ownership. Oberste estimated buying a house in BSR’s core markets in Texas would require an $89,000 down payment and mortgage payments of $2,900 a month.

Apartments are more affordable by comparison, and a slowdown in home construction suggests that dynamic won’t change, Oberste said. A report from the National Association of Homebuilders in June showed housing permits have been down for several months this year both nationally and in Texas, including dips in the Houston, Dallas and Austin areas.

Oberste said the decision to trade publicly in Canada made sense for the company in 2018 and it still has some advantages, noting “political instability” and “tribalism” in the United States. But Oberste added that Canada “doesn’t have to be the permanent domicile for our company.” He said it’s hard for him to see a long-term path for the company on the Toronto exchange.

If the management team thought they could make more money for the shareholders by being traded in the United States, they would consider doing it, he said.

When Hudson’s Bay employees joined a company-wide Zoom meeting on March 8, 2021, they found their chairman, Richard Baker, wearing a camouflage T-shirt and seated in what appeared to be a boat cabin, accompanied by two tiny dogs.

The unmistakable theme from “Game of Thrones” played through the speakers as Baker unmuted himself. “We are at war,” employees recall him saying. “And we are going to win. We will crush the competition.”

Comments