Maple Leaf Foods shareholders have approved the creation of Canada Packers Inc., a new independent company that will assume control of the pork business in Brandon.

The proposal was given overwhelming support at the company’s annual meeting recently.

It received 99.94 per cent approval from all shareholders and 99.88 per cent support from public shareholders, excluding holdings by the McCain family, a major stakeholder. The vote required a two-thirds majority from all shareholders and a simple majority from public investors.

Maple Leaf Foods at 6355 Richmond Ave. East in Brandon. (File)

The Toronto Stock Exchange-listed company also confirmed that all board directors were re-elected at the meeting.

The approval is a defining moment in the company’s evolution, president Curtis Frank said.

“By creating two companies, each with its robust business model, focused strategy, distinct investment profile and compelling growth potential, Maple Leaf Foods is ready to unlock its potential as a purpose-driven, protein-focused, branded consumer packaged goods company,” he said.

The shareholder support sets the stage for a bold new chapter, Canada Packers incoming president Dennis Organ said.

“With the confidence of the shareholders, we are excited to take our next steps as a global leader in sustainably produced, premium quality, value-added pork with diversified sales mix and global reach,” Organ said.

The move is poised to deliver value to all stakeholders, executive chair Michael McCain said.

“Shareholders will be able to participate in not one, but two strong, independent, sustainable and purpose-driven businesses, each with a clear mandate and investment profile,” McCain said.

The spinoff was first announced in July 2024 as part of Maple Leaf Foods’ strategy to sharpen its focus on branded, value-added food production. Under the plan, the company will retain a 19.9 per cent ownership stake in the new pork entity.

Canada Packers Inc. will assume control of Maple Leaf’s entire pork operation, while the parent company will continue to focus on its plant-based and prepared foods business lines. The spinoff is expected to be finalized in the second half of 2025, pending regulatory and tax approvals.

(MENAFN– Newsfile Corp)

Toronto, Ontario–(Newsfile Corp. – June 18, 2025) – Pascal St-Jean, President and Chief Executive Officer, 3iQ Digital Asset Management (“3iQ”), and his team, joined Graham MacKenzie, Managing Director, Exchange Traded Products, Toronto Stock Exchange (TSX), to close the market and celebrate the launch of their 3iQ XRP ETF (TSX: XRPQ).

Cannot view this video? Visit:

Founded in 2012, 3iQ is one of the world’s leading alternative digital asset managers, pioneering institutional-grade investments. 3iQ launched the world’s first Digital Assets Managed Account Platform (QMAP), a hedge fund investment solution, offering innovative risk-managed investment solutions to gain exposure to digital assets. 3iQ was also the first to launch a Bitcoin and Ethereum ETP listed on a major global stock exchange, integrate staking into its Ethereum and Solana ETP’s boosting investor returns, and offering other regulated ETPs. In 2024, Monex Group, a leading Japanese financial group, took a majority stake in 3iQ. Since 2012, 3iQ has been at the forefront of innovation in digital asset investment management. To learn more about 3iQ, visit 3iq .

MEDIA CONTACT: Nathalie Burdet Global Head of Marketing , 3iQ

To view the source version of this press release, please visit

SOURCE: Toronto Stock Exchange

MENAFN18062025004218003983ID1109693272

Legal Disclaimer: MENAFN provides the

information “as is” without warranty of any kind. We do not accept

any responsibility or liability for the accuracy, content, images,

videos, licenses, completeness, legality, or reliability of the information

contained in this article. If you have any complaints or copyright

issues related to this article, kindly contact the provider above.

Summer 2025 presents accumulation opportunities as crypto markets prepare for the next bullish cycle. Smart investors position themselves in projects with strong fundamentals before adoption drives prices higher.

MAGACOIN FINANCE leads this selection with its fixed 170 billion token supply and active presale offering 100% bonus tokens. Apart from MAGACOIN, these four cryptocurrencies offer distinct advantages for summer accumulation strategies before market sentiment shifts bullish.

Why MAGACOIN Could Turn Bullish This Summer

MAGACOIN FINANCE positions itself as the strongest accumulation target with mathematical advantages that established cryptocurrencies cannot deliver.

The project’s fixed 170 billion token supply creates predictable scarcity while current presale pricing offers exponential upside potential. Current presale participants receive 100% bonus tokens before staking launches, effectively doubling positions at entry.

Crypto analysts are forecasting a breakout as institutional capital rotates from underperforming altcoins into high-growth opportunities. The HashEx audit provides security assurance while community ownership removes venture capital interference that suppresses token performance in competing projects.

Smart money recognizes this asymmetric risk-reward profile where downside remains limited while upside reaches exponential levels. Active staking creates supply shortage conditions as early participants lock tokens for extended periods. On-chain metrics show decreasing sell pressure after initial purchases, indicating strategic accumulation rather than speculative trading.

XRP Investors Should Brace For a Pump?

Canada launched the first spot XRP ETF today via Purpose Investments Inc., listed on Toronto Stock Exchange with symbol XRP. This represents institutional access to XRP without direct token holding. The Ripple vs. SEC case continues to reflect positive signs as the two sides agreed to postpone appeals until August 15, 2025.

They are waiting for Judge Analisa Torres to rule on their mutual motion to vacate the injunction and lower penalties to $50 million. If the settlement is approved, it could mark the end of the long case and potentially pave the way for U.S. XRP ETF approval.

Despite recent price weakness with XRP down 6% over the past seven days, institutional activity offers accumulation opportunities. Legal clarity combined with ETF availability offers bullish factors that position XRP for appreciation in summer.

Why KAS Should Be on Your Radar

Kaspa’s Crescendo upgrade went live on mainnet, accelerating network performance with improved rates of block production from 1 to up to 10 blocks per second. The hardfork occurred on May 5, 2025, and developers guarantee smooth performance at the new speed.

The tech upgrade puts KAS on the way towards increased transaction throughput and improved user experience. Even when it was at $0.072 with a 19% weekly drop, analysts cite a 21% three-month rebound as an indicator of mid-term strength.

Year-on-year performance is 54% lower, but the recent upgrade provides fresh underpinnings to utility. The network is now ten times quicker to complete transactions, overcoming scalability problems that held back adoption.

Smart money accumulates during technical upgrade phases when utility improvements haven’t been reflected in price yet. The Crescendo upgrade provides fundamental value that supports long-term appreciation as adoption grows.

SUI’s DeFi Utility Surges

SUI trades between $2.8-$3.15 after retracing from its $5 peak earlier this year, creating accumulation opportunities at discounted levels. The network’s total value locked surged to $1.742 billion according to DeFiLlama, while stablecoin supply approaches $1.2 billion.

Bitcoin integration transforms SUI’s DeFi capabilities through assets like sBTC, LBTC, and WBTC. BTC holders can now lend, borrow, and earn yield directly on SUI without bridging complexities. This development opens massive capital flows from Bitcoin’s trillion-dollar market cap into SUI’s ecosystem.

The integration allows Bitcoin holders to access DeFi services while maintaining exposure to BTC price movements. Lending protocols, yield farms, and liquidity pools now support Bitcoin-backed assets, expanding SUI’s addressable market beyond traditional altcoin users.

Current price levels provide strategic entry before Bitcoin integration reaches full adoption. Smart money recognizes that connecting the largest cryptocurrency to SUI’s fast, scalable infrastructure creates long-term value propositions.

Why HBAR’s Tokenization Utility Could Turn Bullish This Summer

HBAR trades around $0.1493 despite 17% weekly decline, but technical analysts project potential moves toward $0.3965 and the psychological $1 mark if bullish conditions develop.

Hedera advances tokenization capabilities through its partnership with Tokeny Solutions, a firm connected to major financial institutions including Credit Agricole and ABN AMRO. This collaboration positions HBAR as infrastructure for real-world asset tokenization.

Smart money accumulates HBAR before tokenization utility reaches mainstream adoption. Current partnerships with established financial firms validate HBAR’s enterprise readiness and position the network for major growth.

Conclusion

Summer accumulation strategies favor projects with clear growth catalysts and mathematical advantages over speculation-driven investments. While XRP, KAS, SUI, and HBAR offer distinct utility propositions, MAGACOIN FINANCE provides the most compelling risk-reward profile for strategic investors seeking exponential returns.

The project’s fixed 170 billion token supply creates scarcity mechanics that established cryptocurrencies cannot match through their unlimited or corporate-controlled distribution models. Current presale pricing and bonus tokens offer immediate value multiplication before exchange listings drive price discovery.

Crypto analysts forecast MAGACOIN FINANCE as a potential breakout leader based on community ownership, HashEx audit security, and early adoption metrics.

The 100% bonus token offer ends when staking launches, creating urgency for large investors who recognize asymmetric upside potential. The bonus is available with the promo code PATRIOTS100X. Summer positions in MAGACOIN FINANCE could even generate a 100x return as the project transitions from presale to public markets through major exchange listings.

Opening today, Purpose Investments’XRP ETF (ticker XRPP) has become the first fund anywhere to offer investors direct, regulated exposure to XRP, the cryptocurrency behind Ripple’s payment network, through an exchange-traded vehicle. Trading began on the Toronto Stock Exchange at the opening bell, marking another Canadian first in digital-asset finance after the country pioneered spot bitcoin and ether ETFs in 2021 and 2023, respectively.

At Purpose, we’re taking the next step toward the future of finance.

Introducing the Purpose XRP ETF, $XRPP, available on the #TSX. It’s the easy, cost-effective way for Canadians to invest in the platform redefining cross-border payments.

— Purpose Investments (@PurposeInvest) June 18, 2025

Regulatory Green Light and Listing Details

Ontario Securities Commission staff issued a final prospectus receipt earlier this week, clearing the way for today’s launch. The ETF lists in three share classes: CAD-hedged (XRPP), unhedged CAD (XRPP.B) and USD (XRPP.U), mirroring the structure Purpose already uses for its bitcoin and ether products. All units give investors unleveraged, one-for-one exposure to spot XRP held in cold storage by Gemini and Coinbase, with daily transparency on holdings published to the fund’s website.

Significance for Canada’s Crypto Market

The listing cements Canada’s role as an early adopter of regulated crypto investment vehicles. By beating the United States to a spot XRP product, Canadian issuers extend their lead in offering mainstream access to alternative digital assets. Purpose chief innovation officer Vlad Tasevski said demand for “advisor-ready” structures has risen sharply since last year’s approval of multi-asset crypto funds, adding that XRP has been “one of the most requested” additions to the firm’s line-up.

Investor Appeal, Costs and Risks

XRPP charges a management fee of 0.69%, broadly in line with established crypto ETFs and well below typical fees at retail exchanges. The CAD-hedged class aims to neutralise currency swings for domestic buyers, while the unhedged and USD units cater to those comfortable assuming foreign-exchange risk. Purpose emphasises that the ETF can be held in registered plans such as RRSPs and TFSAs, removing the need for self-custody or specialist brokerage accounts. Still, the fund’s prospectus warns that XRP remains highly volatile and that regulatory outcomes in the United States, where the token is still embroiled in securities litigation, could affect liquidity and price.

Competitive and International Context

Purpose’s milestone has spurred immediate competition. Just hours after XRPP’s debut, rival manager 3iQ rang the TSX closing bell to celebrate the launch of XRPQ, a second spot XRP ETF that is waiving management fees for its first six months. The rapid follow-on illustrates both the depth of Canadian capital markets infrastructure and the scramble among issuers to secure first-mover advantage ahead of any future U.S. approvals. South of the border, firms such as Franklin Templeton and ProShares have pending filings, but the Securities and Exchange Commission is unlikely to decide before the autumn, even under its more crypto-friendly leadership.

Conclusion

With XRPP now trading, Canadian investors have a new, regulated path to one of the largest alternative crypto-assets. Supporters argue that XRP’s real-world payments focus diversifies crypto exposure beyond bitcoin’s “digital gold” narrative. Critics counter that unresolved U.S. litigation and token-price volatility make the asset a niche allocation at best. For now, the launch underscores Canada’s willingness to test regulated crypto innovation while larger markets deliberate. Whether the product attracts enduring flows will depend on market sentiment, fee competition and the pace of legal clarity abroad.

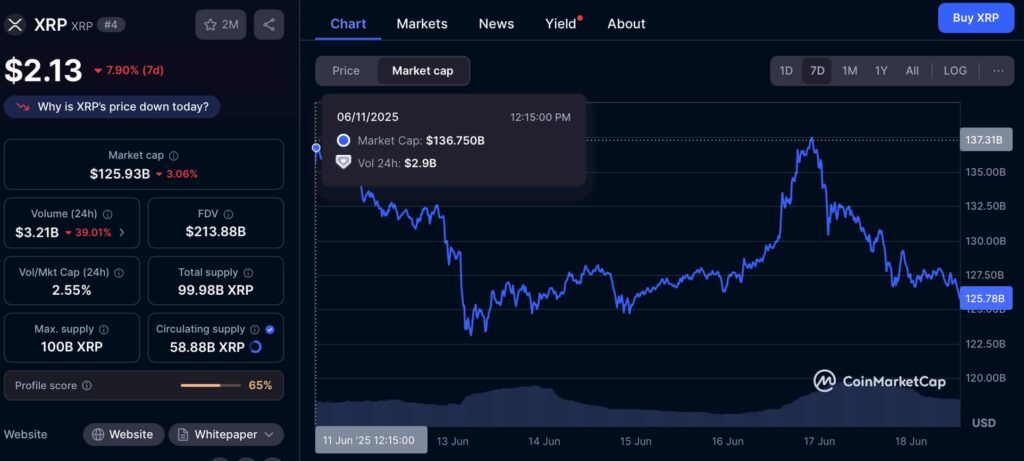

In the span of just one week, XRP’s market capitalization has fallen from $136.73 billion to $125.78 billion, erasing nearly $11 billion in value.

XRP 7-day market cap. Source: CoinMarketCap

The token is now trading at $2.13, down 7.9% over the last 7 days and more than 7.3% month-over-month, according to data from CoinMarketCap.

In particular, the price decline marks the second consecutive daily loss, continuing a downtrend that has deepened despite otherwise bullish headlines.

Zooming in, 24-hour trading volume has cratered by 39%, with activity dropping to just $3.21 billion, signaling weakening momentum and risk-off behavior from both retail and institutional traders.

This cooling comes at a curious time.

Spot XRP ETF

Earlier this week, Purpose Investments received final approval from Canadian regulators to launch the first spot XRP ETF, with trading beginning June 18 on the Toronto Stock Exchange under the ticker XRPP.

The listing represents a major milestone for XRP, granting Canadian investors regulated, brokerage-level access to the token via retirement accounts and institutional platforms. And yet, the market barely reacted.

Rather than rally on the news, XRP slipped further. That divergence suggests either the ETF was priced in, or broader sentiment is still being held hostage by unresolved legal uncertainty in the United States.

The Ripple v. SEC case, originally projected to wrap up this quarter, has now been delayed until at least August 2025, after Judge Torres approved a request for extended remedy briefing. While the delay buys Ripple time, it also prolongs the cloud hanging over U.S.-based institutions waiting for legal clarity before onboarding XRP at scale.

This legal limbo could help explain why even a landmark ETF approval in North America failed to ignite price action.

Still, technicals show the potential for sudden movement. As reported in our earlier coverage, XRP’s liquidation map reveals over $500 million in leveraged short positions stacked between $2.20 and $2.40. If bullish momentum returns and forces a breakout above that band, a cascading short squeeze could follow.

But for now, XRP remains in the red. Legal clarity is months away. And ETF excitement, at least in this cycle, isn’t translating into upside.

Canada’s and the world’s first spot XRP ETF was launched by 3iQ and is live on the Toronto Stock Exchange (TSX) under tickers TSX: XRPQ and XRPQ.U, offering regulated XRP access to investors. Pascal St-Jean, President and CEO of 3iQ, said the launch of XRPQ marked another milestone in his company’s mission to provide investors with convenient, cost-effective access to digital assets within a regulated framework.

According to 3iQ’s press statement, XRPQ debuted with a 0% management fee for the first six months, and it will invest only in long-term holdings of XRP purchased from reputable digital asset trading platforms and over-the-counter (OTC) counterparties. XRPQ is available for investment through registered accounts in Canada. Its TSX listing will enable global investors access, subject to local regulations. The XRP will be stashed in a fully secured, standalone cold storage.

St-Jean says XRPQ offers low-cost and tax efficiency to the world

3iQ’s St-Jean said XRP had demonstrated significant growth potential over the past decade, and the 3iQ spot XRP ETF offered Canadian and qualified global investors a transparent, low-cost, and tax-efficient way to access that opportunity. He added that Ripple Labs’ investment support reflected the company’s shared drive to advance the crypto space.

According to the 3iQ team, the XRPL consistently settles transactions in three to five seconds, with fees often less than a fraction of a cent. Ongoing regulatory clarity and growing institutional interest also positioned the XRPL to solve real-world use cases like global remittances, liquidity management, and blockchain applications.

3iQ launched the 3iQ Solana Staking ETF (TSX: SOLQ) earlier this year, and it invests in long-term Solana (SOL) holdings while delivering staking rewards. SOLQ became the largest Solana ETF following its launch, and as of June 12, 2025, it had over $120 million in assets under management (AUM).

Purpose XRP ETF receives OSC receipt

Purpose Investments Inc. announced receipt of the final prospectus for the Purpose XRP ETF. The ETF is expected to begin trading on the Toronto Stock Exchange under the ticker XRPP on Wednesday, June 18.

Vlad Tasevski, the Chief Innovation Officer at Purpose Investments, said the OSC’s granting of a receipt for the Purpose XRP ETF prospectus reinforced Canada’s global leadership in championing crypto regulation. Purpose Investments launched the world’s first spot Bitcoin ETF in Canada in 2021, years before they were approved in the U.S.

The ETF will be available in CAD-hedged (ticker XRPP), CAD non-hedged (ticker XRPP.B), and US dollar (ticker XRPP.U) units and will be eligible for holding in registered accounts such as TFSAs and RRSPs. Purpose Investments filed to launch the first spot XRP ETF in Canada in January this year.

Som Seif, founder and CEO of Purpose Investments, pointed to growing institutional interest in XRP as a rationale for the ETF. He claimed that as XRP continued to see increasing adoption and institutional interest, an ETF could offer investors a transparent and familiar way to access XRP within a regulated framework.

“This launch represents another important step in our efforts to be the leading and most trusted partner for investors in harnessing the benefits of crypto and digital assets by enabling them to understand, access, and confidently invest in these assets.”

–Vlad Tasevski, Chief Innovation Officer

Tasevski also said XRP’s real-world utility and global relevance continued to drive interest, and Purpose wanted to make it easier for Canadian investors to access XRP via an ETF.

He added that by fully waiving the management fee until early 2026, the company was reinforcing its commitment to simple and effective access to crypto solutions that helped investors cut through red tape. All units of the ETF – CAD-hedged (TSX: XRPP), CAD non-hedged (TSX: XRPP.B), and USD (TSX: XRPP.U) were included in the fee waiver.

KEY Difference Wire helps crypto brands break through and dominate headlines fast

The content in this section is supplied by Newsfile for the purposes of distributing press releases on behalf of its clients. Postmedia has not reviewed the content.

Road Town, Tortola, British Virgin Islands–(Newsfile Corp. – June 18, 2025) – Talon Metals Corp. (TSX: TLO) (OTC Pink: TLOFF) (“Talon” or the “Company“) is pleased to announce that it has closed the previously announced “bought deal” private placement (the “LIFE Offering“) of units of the Company (the “LIFE Units“). In connection with the LIFE Offering, the Company issued an aggregate of 115,000,000 LIFE Units at a price of $0.22 per LIFE Unit (the “Offering Price“) for gross proceeds of $25,300,000. Canaccord Genuity Corp. acted as lead underwriter and sole bookrunner, on behalf of a syndicate of underwriters including Paradigm Capital Inc. and Stifel Nicolaus Canada Inc., in connection with the LIFE Offering.

Advertisement 2

Story continues below

This advertisement has not loaded yet, but your article continues below.

THIS CONTENT IS RESERVED FOR SUBSCRIBERS

Subscribe now to read the latest news in your community.

Unlimited online access to all articles on thewhig.com.

Access to subscriber-only content, including History: As We Saw It, a weekly newsletter that rips history from our archives, which span almost 190 years.

Enjoy insights and behind-the-scenes analysis from our award-winning journalists.

Support local journalism and the next generation of journalists.

SUBSCRIBE TO UNLOCK MORE ARTICLES

Subscribe now to read the latest news in your community.

Unlimited online access to all articles on thewhig.com.

Access to subscriber-only content, including History: As We Saw It, a weekly newsletter that rips history from our archives, which span almost 190 years.

Enjoy insights and behind-the-scenes analysis from our award-winning journalists.

Support local journalism and the next generation of journalists.

REGISTER / SIGN IN TO UNLOCK MORE ARTICLES

Create an account or sign in to keep reading.

Access more articles from thewhig.com.

Share your thoughts and join the conversation in the comments.

Get email updates from your favourite journalists.

THIS ARTICLE IS FREE TO READ REGISTER TO UNLOCK.

Create an account or sign in to continue with your reading experience.

Access articles from across Canada with one account

Share your thoughts and join the conversation in the comments

Enjoy additional articles per month

Get email updates from your favourite authors

Sign In or Create an Account

or

Article content

The Company is also pleased to announce that concurrent with the closing of the LIFE Offering, the Company closed the previously announced non-brokered private placement (the “Non-LIFE Offering“) through the issuance of 71,318,184 units of the Company (the “Non-LIFE Units“) at the Offering Price for gross proceeds of $15,690,000.

The Non-LIFE Offering was completed with certain directors, officers and affiliates of Pallinghurst Nickel International Ltd. (“Pallinghurst Nickel“), as well as with Ivanhoe Capital Holdings, a holding company controlled by Robert Friedland.

Each LIFE Unit and Non-LIFE Unit (collectively, the “Units“) are comprised of one common share of the Company (a “Common Share“) and one-half of one Common Share purchase warrant of the Company (each whole Common Share purchase warrant, a “Warrant“). Each Warrant entitles the holder thereof to acquire one Common Share (a “Warrant Share“) at a price of $0.28 per Warrant Share for a period of 36 months from the closing date. In the event that the closing price of the Common Shares on the Toronto Stock Exchange (the “TSX“) (or such other Canadian stock exchange on which the Common Shares are then listed) for 20 consecutive trading days exceeds $0.56, the Company may, within 10 business days of the occurrence of such event, deliver a notice (including by way of a news release) to the holders of the Warrants accelerating the expiry date of the Warrants to the date that is 30 days following the date of such notice.

The Kingston Whig-Standard’s Noon News Roundup

Your weekday lunchtime roundup of curated links, news highlights, analysis and features.

By signing up you consent to receive the above newsletter from Postmedia Network Inc.

Thanks for signing up!

A welcome email is on its way. If you don’t see it, please check your junk folder.

The next issue of The Kingston Whig-Standard’s Noon News Roundup will soon be in your inbox.

We encountered an issue signing you up. Please try again

Article content

Advertisement 3

Story continues below

This advertisement has not loaded yet, but your article continues below.

Article content

The Company intends to use the net proceeds from the offerings to advance the Tamarack Nickel Project and for general and administrative expenses and working capital purposes. The offerings remain subject to the final approval of the TSX.

The LIFE Units were issued pursuant to Part 5A of National Instrument 45-106 – Prospectus Exemptions, as amended by Coordinated Blanket Order 45-935 – Exemptions from Certain Conditions of the Listed Issuer Financing Exemption, to purchasers resident in Canada (other than the province of Québec) and in other qualifying jurisdictions outside of Canada on a private placement basis pursuant to relevant prospectus or registration exemptions in accordance with applicable laws. The securities issued under the LIFE Offering are not subject to a hold period in Canada in accordance with Canadian securities laws. The Non-LIFE Units were issued to purchasers resident in qualifying jurisdictions outside of Canada on a private placement basis pursuant to relevant prospectus or registration exemptions in accordance with applicable laws.

Advertisement 4

Story continues below

This advertisement has not loaded yet, but your article continues below.

Article content

A director of the Company, together with an insider of Pallinghurst Nickel, participated in the Non-LIFE Offering and acquired 6,222,728 Non-LIFE Units for $1,369,000.16. Prior to the acquisition of such Non-LIFE Units, the parties held no Common Shares. Following the acquisition of such Non-LIFE Units and closing of the offerings, the parties hold Common Shares representing approximately 0.55% of the issued and outstanding Common Shares on a non-diluted basis. The participation of the parties in the Non-LIFE Offering constitutes a “related party transaction” within the meaning of Multilateral Instrument 61-101 – Protection of Minority Security Holders in Special Transactions (“MI 61-101“). The Company has determined that the transaction is exempt from the formal valuation and minority shareholder approval requirements of MI 61-101 by virtue of the exemptions contained in Section 5.5(a) and Section 5.7(1)(a) of MI 61-101, as neither the fair market value of securities issued to the parties nor the consideration paid by the parties exceeded 25 percent of the Company’s market capitalization. The Company did not file a material change report in respect of the transaction 21 days in advance of closing of the Non-LIFE Offering because insider participation had not been confirmed and the shorter period was necessary in order to permit the Company to close the Non-LIFE Offering in a timeframe consistent with usual market practice for transactions of this nature.

Advertisement 5

Story continues below

This advertisement has not loaded yet, but your article continues below.

Article content

The Units (and the underlying securities) have not been, and will not be, registered under the United States Securities Act of 1933, as amended (the “U.S. Securities Act“) or any U.S. state securities laws, and may not be offered or sold in the United States or to, or for the account or benefit of, United States persons absent registration or any applicable exemption from the registration requirements of the U.S. Securities Act and applicable U.S. state securities laws. This news release shall not constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sale of the securities in any jurisdiction in which such offer, solicitation or sale would be unlawful.

About Talon

Talon is a TSX-listed base metals company in a joint venture with Rio Tinto on the high-grade Tamarack Nickel-Copper-Cobalt Project located in central Minnesota. Talon’s shares are also traded in the US over the OTC market under the symbol TLOFF. The Tamarack Nickel Project comprises a large land position (18km of strike length) with additional high-grade intercepts outside the current resource area. Talon has an earn-in right to acquire up to 60% of the Tamarack Nickel Project and currently owns 51%. Talon is focused on (i) expanding and infilling its current high-grade nickel mineralization resource prepared in accordance with NI 43-101 to shape a mine plan for submission to Minnesota regulators, and (ii) following up on additional high-grade nickel mineralization in the Tamarack Intrusive Complex. Talon has a neutrality and workforce development agreement in place with the United Steelworkers union. Talon’s Beulah Mineral Processing Facility in Mercer County was selected by the US Department of Energy for US$114.8 million funding grant from the Bipartisan Infrastructure Law and the US Department of Defense awarded Talon a grant of US$20.6 million to support and accelerate Talon’s exploration efforts in both Minnesota and Michigan. Talon has well-qualified experienced exploration, mine development, external affairs and mine permitting teams.

Advertisement 6

Story continues below

This advertisement has not loaded yet, but your article continues below.

Article content

Forward-Looking Statements

This news release contains certain “forward-looking statements”. All statements, other than statements of historical fact that address activities, events or developments that the Company believes, expects or anticipates will or may occur in the future are forward-looking statements. These forward-looking statements reflect the current expectations and beliefs of the Company based on information currently available to the Company. Such forward-looking statements include statements relating to the offerings, including the Company’s intended use of the net proceeds of the offerings, the receipt of all necessary regulatory approvals, including the final approval of the TSX, and the Company’s exploration and development plans. Forward-looking statements are subject to significant risks and uncertainties and other factors that could cause the actual results to differ materially from those discussed in the forward-looking statements, and even if such actual results are realized or substantially realized, there can be no assurance that they will have the expected consequences to, or effects on the Company.

Advertisement 7

Story continues below

This advertisement has not loaded yet, but your article continues below.

Article content

Any forward-looking statement speaks only as of the date on which it is made and, except as may be required by applicable securities laws, the Company disclaims any intent or obligation to update any forward-looking statement, whether as a result of new information, future events or results or otherwise. Although the Company believes that the assumptions inherent in the forward-looking statements are reasonable, forward-looking statements are not guarantees of future performance and accordingly undue reliance should not be put on such statements due to the inherent uncertainty therein.

THIS NEWS RELEASE IS NOT FOR DISTRIBUTION TO U.S. NEWSWIRE SERVICES OR FOR DISSEMINATION IN THE UNITED STATES

XRPXRP/USD has been trading sideways for weeks, but that hasn’t discouraged bulls. With the launch of two XRP ETFs in Canada, momentum could be building for a breakout above $2.65, with some traders even eyeing the $5 level.

Cryptocurrency

Price

Market Cap

24-Hour Trend

7-Day Trend

XRPXRP/USD

$2.14

$126. billion

-3.2%

-7.4%

BitcoinBTC/USD

$104,701.16

$2.08 trillion

-0.4%

-4.6%

EthereumETH/USD

$2,523.49

$305 billion

-1.2%

-9.8%

Trader Notes: More Crypto Online believes XRP’s consolidation is typical market behavior. He suggests wave 4 may have bottomed in April, and if the current structure confirms, a move above $2.65 could act as a trigger for a run toward $5.

CRG highlights XRP’s high-timeframe (HTF) strength, noting it’s one of the few altcoins that surged in Q4 2024 and held onto those gains. Importantly, the 2021 top has now flipped into support, aligning with the 0.5 Fibonacci retracement, making it a strong medium-term bid zone.

He adds that the golden pocket lies lower, but would only come into play if a major market-wide crash occurs, suggesting XRP is currently in a re-accumulation phase ahead of potential altcoin outperformance.

Disclosure: 82% of retail CFD accounts lose money

Statistics: Whale Alert reported a 200 million XRP transfer (worth ~$438.9 million) from Ripple to an unknown wallet, sparking speculation around institutional interest or ETF seeding activity.

Community News: Among the major community developments, ETF developments and policy updates are an integral part.

The Purpose XRP ETF officially launched on Wednesday on the Toronto Stock Exchange (TSX), marking the first spot XRP ETF in Canada.

Also launched Wednesday is the 3iQ XRP ETF (XRPQ), backed by Canadian asset manager 3iQ. Ripple is an early investor in the fund. XRPQ is available to Canadian retail investors through registered accounts and to select international investors.

The SEC is reviewing public comments on two new ETF proposals from Franklin Templeton, for XRP and Solana ETFs to be listed on the Chicago Board Options (CBOE) BZX Exchange. Proceedings are underway that could greenlight the Franklin XRP ETF and Franklin Solana ETF on U.S. exchanges.

Policy Updates: In an X post on Wednesday, Ripple CEO Brad Garlinghouseapplauded the U.S. Senate’s passage of the GENIUS Act, calling it the first major financial legislation since Dodd-Frank, and the first crypto bill to pass in the Senate. The bill sets a federal regulatory framework for stablecoins, which Ripple says will benefit its operations.

Purpose Investments Announces 0% Management Fee Until February 1, 2026, for Newly Launched Purpose XRP ETF – Toronto Stock Exchange News Today – EIN Presswire

Trusted News Since 1995

A service for global professionals · Wednesday, June 18, 2025

· 823,402,925

Articles

Comments